Investment Notes

FrankieOne: Seed to Series A

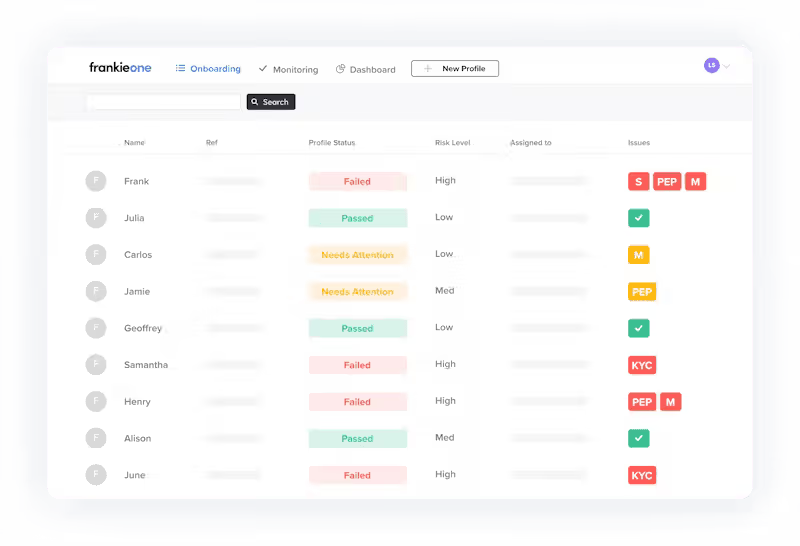

FrankieOne provides customers with a single API to better manage KYC/AML and Fraud. Its integrated platform delivers a unified view of end customers and unlocks data-led decision-making and workflow automation for compliance, operations, audit, and risk.

FrankieOne (or just "Frankie") recently announced a A$20 million Series A round co-led by US VC fund Greycroft and Sydney-based Airtree Ventures, with participation from Harry Stebbing's 20VC in the UK, Reinventure, Mantis Ventures in the US, high profile executives from global Fintechs such as Robinhood and Public, and follow-on investment from Tidal and other existing investors. This brings the company's total funding to just under $23 million.

Frankie's announcement comes one week after one of its competitors, Alloy, announced a US$100 million Series C round at a whopping US$1.35 billion valuation, suggesting this is a hot sector to be backing right now. But what did we know at the time we invested in the Early Seed round two-and-a half years ago? Let's take a look at how our investment thesis from May 2019 has stood up against the world we know today.

Markets with tailwinds

FrankieOne capitalizes on a data integration & orchestration opportunity within the financial services sector. Existing point solutions are often decentralized, requiring multiple integrations (and in some cases, they completely fail to integrate with legacy systems), and provide poor visibility of the customer to financial service providers....and a broken user experience to boot.

And yet, KYC ("Know Your Customer"), AML ("Anti-Money Laundering") and Fraud prevention solutions are mission critical when onboarding new customers and monitoring BAU transactions. The cost of not having adequate tooling and protection can be hugely material to a financial services provider in terms of cyber fraud, as well as revenue left on the table.

We have seen this act play out in a material way in the consumer services sector when Twilio (and similar service providers) saw adoption at scale to provide non-core capabilities to customer tech stacks.

Our thesis: With the build out of open banking and digitally native financial services companies, there is a huge opportunity for the emergence of an automated aggregator for critical services that feed into these banking stacks. The first wave of this is KYC, AML, Identity Verification and Transaction Monitoring.

Products that change the game

Frankie connects compliance and risk data sources to a single API that unifies how its customer base (which includes the likes of Westpac, AfterPay, crypto exchanges, utility companies, wealth management platforms, lending institutions etc.) onboard and monitor their customers, meeting global regulatory requirements.

Frankie's product currency (how it is directly attributable to a measurable outcome for its customer) is two-fold:

(1) A higher "pass-through rate" (the % of new customers that are verified & approved for onboarding) that it delivers by leveraging hundreds of data sources and utilizing its intelligent decision engine to solve for missing information across multiple sources → this increases revenue for the customer and saves the cost and complexity that accompanies manual intervention.

(2) A unified view of consumers at the end customer level (not by product, for example), delivering a better onboarding experience to consumers and a more secure means of ongoing monitoring → this improves consumer satisfaction & retention, and eliminates the multi-step process currently undertaken to stitch together a holistic view of an end customer (e.g. the customers of a bank).

Founders that hustle

Two key attributes we look for in founders are (1) whether they have a unique insight or experience with the problem space they’re trying to solve, and (2) whether they employ a data-driven approach to building a business (how they assess the market opportunity, acquire customers and establish a test & iteration culture).

On the first point, co-founders Simon Costello and Aaron Chipper were FrankieOne’s first customers. Let me explain this circular reference — Simon’s journey with Frankie began with him building the foundations of a neobank (branded “Frankie”) for the Australian market in 2018.

It was during this process that Simon & Aaron experienced a lack of plug & play solution to conduct KYC and AML for new customers. Even when building a financial services company from the ground up — one that would not be encumbered by legacy systems (in comparison to a large Australian bank, for example) — they could not find a solution that delivered what they wanted. There were individual data sources to connect to, but doing so left revenue on the table and did not help deliver an amazing experience to the end customer (an absolute must for any new consumer product focused on Millenials). Simon even delved into the business banking sector only to realize the same applied to KYB (“Know Your Business”) — the industry was stiffened by legacy systems and manual processes (KYB is now a fast-growing component of FrankieOne's product suite).

This leads me to the second point. I believe it was back in 2016, while Simon was still at the helm of a fast-growing Fintech in SE Asia, that he flew to Sydney for a conference to begin his market research on the emerging Fintech landscape in Australia. Having previously lived in the UK, he'd seen the rise of digital challenger banks such as Monzo and I'll never forget Simon sending me the link to its crowdfunding page (I note Monzo is now valued north of A$2 billion!). When Simon moved back to Australia with his vision in mind, I watched him meticulously conduct market studies with carefully crafted user groups to identify exactly where the pain points persisted.

Simon's decision to pull the launch of Frankie, in exchange for the RegTech version of the business we know it to be today, was not one taken lightly — the legals had been finalized, the wireframes for the consumer app built and commitments secured for a large angel round...but it wasn't the multi-billion dollar global opportunity he saw with FrankieOne. Simon's ability to put pens down at the final hour was supported by his data-driven approach to decision making and only served to build even more confidence with investors in his execution capabilities when he came back to fundraise for FrankieOne.

We backed FrankieOne at the earliest stage of Seed, when it was pre-launch. We had huge conviction in the market but it’s fair to say we put our chips on Simon & Aaron, founders with a clear vision and the discipline to truly test the market and iterate.

Seed: landing a compelling business model and strong product-market-fit

Frankie's Seed Phase comprised two rounds — the first was pre-launch and the second was just as the company was going live with its first handful of customers.

One of Frankie's first tasks was determining the best pricing model for the business and its customers. Frankie went to market with a SaaS consumption model — customers are charged a SaaS fee that gives them access to Frankie's software in addition to a transaction fee charged for each API call (which equates to product usage, across any of: KYC, AML, KYB, IDV and new products to come). The transaction fee (or consumption-based component) cost per unit varies by product and the volume of usage.

In terms of achieving PMF, one of Frankie's most compelling attributes has been the inbound nature of its customer base. The team acquired its first +50 customers through inbound leads and referrals → a clear indication that people were proactively searching for a solution to a problem they were facing. In order to facilitate this flywheel, the company launched a website with crystal clear messaging around its core capabilities and the problem it solved. The team also focused on 'landing' with one product (e.g. KYC) as the likelihood that a customer would expand to another product (e.g. AML) was high once Frankie earned a customer's trust. This simplified GTM messaging reduced complexity in the sales pitch as well as made the decision-making process for the customer a lot more straightforward (vis-a-vis selling a suite of products upfront).

Series A: a scalable GTM model and a defensible moat

In order to build next-round investor confidence that Frankie was positioned for scale by the time it launched its Series A round, we workshopped a list of prioritized 'Series A proof points' to help focus resources & time. The team was exceptional at systematically ticking these off one by one over the 12 months that followed.

A big question thrown around during white boarding sessions was "how can Frankie get its customers up and running quicker". This was especially relevant for start-up and mid-market customer segments. Frankie released a Stripe-like widget enabling customers to create their own customized onboarding flows with only a couple lines of code, auto-populating personalized screens that would otherwise have taken weeks to build.

Frankie also focused on shortening the TTV ("time-to-value") for its customers by rolling out Smart UI onboarding screens for its end customers, which improved usability and resulted in a much timelier increase in the pass-through rate for Frankie's customer.

To overseas markets and beyond

To date, FrankieOne has focused its GTM efforts on Australia but this hasn't stopped it from generating > 40% of its revenue from international markets. For starters, some of Frankie's largest customers, acquired in Australia, have pulled the company into overseas markets in which they operate, based on the clear product currency delivered by Frankie on domestic soil. The company also landed Zipmex, a fast-growing cryptocurrency exchange based in Southeast Asia. Frankie has connected data sources in more than 46 countries (and counting), setting the stage for further global domination.

A big part of this next phase in the company's growth will be to proactively enter key geographical markets. One of the core differentiators between Frankie and its competitors around the globe stems from the conscious approach it took on Day One, to address a breadth of customer by vertical and size, ensuring compliance with the largest of banks down to the smallest of Fintech startups.

A note on the Fintech infrastructure thematic

The definition of a Financial Services Provider is evolving to include almost anyone as the demonstrated acceleration of embedded finance reshapes the financial services industry (noting embedded finance is projected to grow by 922% between 2020 and 2025). We talk about the non-core (but mission critical) element of KYC/AML and Fraud Monitoring across Frankie's existing customer base — the dynamic of this relationship only intensifies when you extend Frankie's applicability to any company with an embedded finance offering, where the core focus of the tech stack could be on travel or e-commerce, sitting well outside the realm of financial technology.

Payment services was the first to be embedded, though we have now seen the layering in of more complex capabilities (e.g. FX, lending and insurance) into the tech stacks of embedded finance providers alike.

Frankie becomes a required addition to the primary embedded financial service into the tech stack of non-financial products.

It is the growth of embedded finance up until today that has fueled the proliferation of Fintech giants like Stripe and Square and is poised to have a multiplier effect on the success of companies like FrankieOne.

We look forward to continuing to support the FrankieOne team. If you're a visionary founder who is ready to make waves, please reach out via our website.